Insurance and Guarantees for Successful Infrastructure Risk Mitigation in Asia

Insurance and guarantees: One important key to successful infrastructure risk mitigation in Asia

Infrastructure projects have been crucial in Asia’s development journey, spurring growth, tackling poverty, and increasing connectivity. The demand for infrastructure will not let up; the Asian Development Bank estimates that Asia requires an investment of US$1.7 trillion every year until 2030 1.

To help plug this gap and better manage project risks, the private sector must take on a larger role - but project structures need to first demonstrate good risk allocation principles, measures, and support arrangements. How can projects capture interest from investors with the right insurance and guarantees strategies?

Leveraging insurance and other risk mitigation instruments

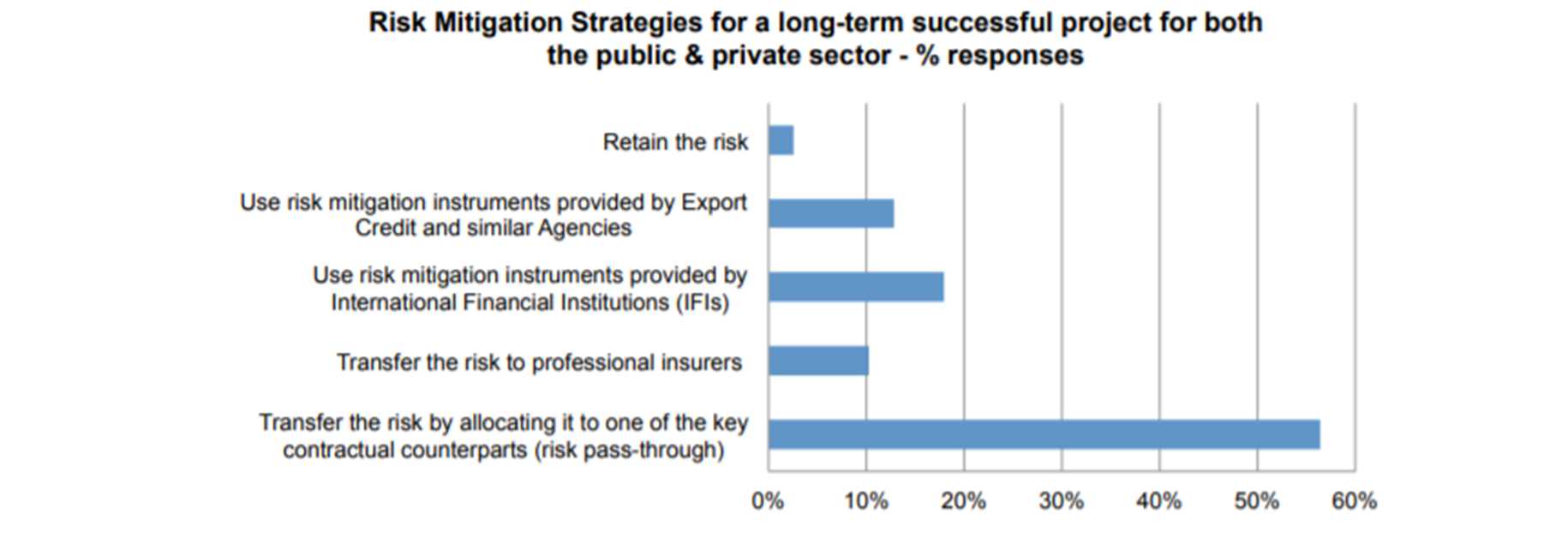

Risk management strategies can be classified under the broad categories of retain, reduce, and transfer. The World Economic Forum’s 2016 report found that the most popular risk mitigation strategy is to transfer risk to contractual counterparts, with over 50% of total surveyed respondents utilising this strategy.

Utilisation of Risk Mitigation Strategies

This strategy is especially useful for technical and construction risks, which can be well mitigated by specialised operators which focus on engineering, procurement and construction, and operation & maintenance aspects.2 Transferring such risks to the counterparties best able to handle them can generate incentives for effective project delivery.

According to the report, other risk mitigation strategies were less commonly used, achieving utilisation rates of lower than 20%. These include insurance and guarantees provided by development finance institutions (DFIs), private insurers, and export credit agencies (ECAs). This implies that projects which do not diversify their risk strategies are unable to reap the benefits of diverse risk mitigation strategies when designing a risk structure, and may end up with a less-than-optimal risk allocation.

Lowering overall project risk and crowding in the private sector

It would be worthwhile for projects to explore increasing usage of diverse tools such as insurance and guarantees to enable more private sector participation. Insurance products can offer wide and comprehensive coverages that protect against risks that the counterparties involved are not able to control and manage effectively.

Mark Houghton, Head of Political Risk, Credit & Bond, APAC, AXA XL shared that the political and credit risk insurance market is highly effective in mobilising capital for infrastructure projects across the globe.

A wide scope of risks can be covered by insurance, including country and sovereign risks for project sponsors; non-tangible risks such as the breach of key operating contracts by the host government or currency inconvertibility risks; as well as credit risks to encompass non-payment by the project company or be tailored to protect specific cash flows generated by the project.

Insurance companies have also been adapting to meet newer market needs. Mr Houghton highlighted that as projects push the barriers of technological advancement, the private insurance market has developed products that can provide cover for technology risk to ensure debt service can be met, particularly for projects seeking to deploy new or innovative technologies.

The offerings of private insurance can also be complemented by risk mitigation tools from DFIs; these can fill the gaps by providing coverage in areas that the private sector is less equipped to manage.

Insurance also helps to increase DFIs capacity to assist emerging markets. Alexander N. Jett, Senior Investment Specialist (Guarantees), and Dennis Eucogco, Senior Guarantees and Syndications Specialist, from the Asian Development Bank’s (ADB) Guarantees and Syndications Unit shared that ADB also leverages credit insurance to mobilise more of their own funding, helping to increase interest in emerging market deals. ADB is in fact a larger buyer of credit insurance than a seller of guarantees.

DFIs can play multiple roles in a project. They offer a range of risk mitigation instruments including financial guarantees, insurance, and credit enhancement schemes. Given DFIs typical have multiple engagements in the country, there is also a halo effect from DFI involvement, which can act as a lever to crowd in more private sector players for projects. The multiple roles that a DFI plays in a project can also help make guarantees more well-structured. For example, ADB’s typical involvement as a lender and guarantor allows project and loan documents to clearly delineate the scope of political risks and allows the guarantee package to adequately address the needs of clients.

One such case study is the Riau power project in Indonesia where, in addition to its own loan, ADB is acting as the lender of record for two commercial lenders, contributing roughly $80 million in commercial financing. These lenders are also covered by an ADB Political Risk Guarantee which covers political risks (war, transferability, expropriation) as well as breach of contract.

Providing comfort to financiers and enhancing overall credit worthiness

The importance of insurance is also echoed by private sector financiers. Surya Bagchi, Global Head of Project and Export Finance at Standard Chartered Bank, shared that “insurance products can be used to target specific risks to provide comfort to financiers. At its most basic form we have used it to address political risks in emerging markets for equity investors as well as lenders in our transactions facilitating longer tenor financing in international currencies. We have used the extended political risk or four-point cover, additionally covering for the risk of contract frustration which can often make the difference to get to a bankable structure with a sustainable financing tenor, that is compatible with the useful life of the underlying infrastructure asset.”

Even for projects that are already attractive to private sector on their own, insurance and guarantees can still bring about further benefits to project owners from financiers such as enabling longer loan tenors or more attractive rates.

Insurance solutions have helped Standard Chartered Bank unlock long tenor project financing in power projects in countries including Ghana, Nigeria, and Bangladesh. Discussions are on-going for certain State-Owned Enterprise transactions in India as well.

Mr Bagchi highlighted, “In Cameroon for instance, we have successfully worked with the World Bank, utilising Political Risk Guarantee structures to facilitate long term local currency lending on a mini-perm basis into Kribi Power with a 7 + 7 year tenor (2011) and more recently, Nachtigal Hydro, with a 7 + 7 + 7 year tenor (2018). Both transactions attracted local financing at rates comparable to Euro-denominated DFI tranches.”

Another tool that can increase the willingness of financiers to offer long tenor project finance loans are the insurance and guarantees provided by Export Credit Agencies (ECAs). Mr Bagchi shared, “Long tenor project finance loans need to balance between achieving good shareholder returns for banks in the face of increasing regulatory capital requirements and facilitating the best pricing for large debt sizes to facilitate sustainable and affordable infrastructure in developing economies. Insurance cover and guarantees from ECAs are a very efficient tool to make project financing loans capital efficient for banks and enable competitive pricing for long tenors and large amounts.”

The true potential of risk mitigation tools for a better infrastructure future

While the current suite of risk mitigation tools in the market already offers a multitude of benefits for infrastructure projects, there is room for these tools to go even further in making infrastructure projects happen.

One possibility is to enable insurance to become a large-scale asset class by creating a system-wide risk insurance platform. This will mobilise significantly greater participation by private sector players, such as institutional investors. From 2011 to 2016, the number of institutional investors in infrastructure has more than doubled 3. A platform can further catalyse the involvement of and unlock more capital from these investors, as suggested by the G20 Eminent Persons Group. Additionally, a platform will also allow for more collaboration between DFIs and investors, enabling DFIs to recycle their capital and free-up their balance sheet to work with more projects 4.

Subnational projects could also benefit from more suitable risk mitigation tools. Increasingly, responsibilities such as ensuring sustainable developments and filling infrastructure deficits are taken on by subnational governments rather than central government agencies, as the former are closer to the ground and have greater incentives and opportunities to think holistically 5. However, current products are still largely geared towards sovereign projects. By widening the scope of traditional insurance to include subnational projects, this will allow the creation of a more dynamic and robust market.

With proper risk mitigation strategies, we can be one step closer to bridging the infrastructure financing gap. Insurance and guarantees are important risk mitigation instruments that have yet been tapped on fully by the market. Getting over the initial barriers of perceived complexity will allow project owners to reap substantial benefits such as crowding in private sector partners and enabling more favourable financing deals.

1 (ADB, 2017)ADB, 2017. Retrieved from: https://www.adb.org/news/asia-infrastructure-needs-exceed-17-trillion-year-double-previous-estimates

2 OECD, 2017. Retrieved from: http://www.oecd.org/daf/fin/private-pensions/Selected-Good-Practices-for-Risk-allocation-and-Mitigation-in-Infrastructure-in-APEC-Economies.pdf

3 WEF, 2016. Retrieved from: http://www3.weforum.org/docs/WEF_Risk_Mitigation_Instruments_in_Infrastructure.pdf

4 20 Eminent Persons Group, 2018. Retrieved from: https://us.boell.org/sites/default/files/10-3-18_report_of_the_g20_eminent_persons_group_on_global_financial_governance.pdf

5 ADB, 2019. Retrieved from: https://www.adb.org/sites/default/files/publication/485851/adbi-wp921.pdf

This article was collated by Lee Mei Lin and Seth Tan and benefitted from the information and views shared by:

- Alexander N. Jett, Senior Investment Specialist (Guarantees), Asian Development Bank

- Dennis Eucogco, Senior Guarantees and Syndications Specialist, Asian Development Bank

- Mark Houghton, Head of Political Risk, Credit & Bond, APAC, AXA XL

- Surya Bagchi, Global Head of Project and Export Finance at Standard Chartered Bank