Green Finance in Emerging Asia

This article highlights the greater adoption of green projects in the region with an increase of green financing.

The need for green projects, such as sustainable infrastructure and renewable energy, is growing. It is estimated that the average annual demand will be US$200 billion per annum up to 2030 in Asia. Within ASEAN, the annual volume of green financing supply is estimated to have increased to US$40 billion. This article highlights the increasing supply and also attainability of green financing and that this may in turn pave the way for greater adoption of green projects in the region.

Green Activities: Mitigating Social and Environmental Impacts

Asian cities are projected to contribute more than half the rise in global greenhouse gas emissions over the next 20 years if no radical changes are implemented. Low-lying and coastal cities in the Asian region are prone to the rising sea levels, frequent floods and other impacts of climate change. With the effects of climate change becoming increasingly apparent, sustainable projects play a key role in protecting our environment.

Within the Southeast Asia region, the urban population is expected to increase by 90 million up to 2030. Sustainable infrastructure grows in importance as it can mitigate various consequences of rapid growth, such as increasing power consumption, waste generation etc.

Green Bonds and Loans: Rising Popularity

With Singapore’s green bond market standing at more than SGD 6 billion today, the Singapore ecosystem is well-positioned to enable more green bonds. Green loans are also gaining traction. Green loans are a strong feature of the ASEAN market, comprising of 22.5% of the loans in ASEAN. Proceeds from green bonds and loans can be used to finance various environmental and sustainable infrastructure projects, such as renewable energy, energy-efficient buildings and low carbon projects. In 2018, Olam International secured Asia’s first sustainability-linked club loan facility of US$500 million, in which 15 banks were appointed to provide the facility in equal parts. This loan included banks like co-sustainable advisor ING Bank N.V., Standard Chartered Bank, DBS Bank Ltd. and Australia and New Zealand Banking Group Limited. Earlier this year, Sunseap sealed the first green loan of S$50 million with ING Bank N.V. in ASEAN that is compliant with LMA/APLMA Green Loan Principles for rooftop solar projects. Sustainalytics provided a second party opinion on Sunseap's Green Finance Framework. The increasing number of deals involving green finance demonstrates the growing appetite of banks based in the region to support this asset class. Issuances of green loans are recently over-subscribed and some even offer to adjust loan pricing in favour of improved compliance with green benchmarks. These are very positive signs of strong support and demand. Based on Infrastructure Asia’s discussion with the market, there is interest to do more.

Green Buildings: Increasing Focus of the Region

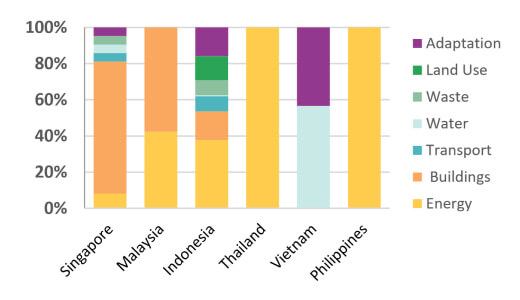

In 2018, over 40% of ASEAN green bonds’ proceeds target low carbon buildings, which is the predominant category for green bond proceeds in the region. In Singapore, given the early adoption of green buildings since the introduction of the Building & Construction Authority’s (BCA) Green Mark Scheme in 2005, green bonds mainly finance buildings.

The report demonstrates that higher percentage of proceeds from green bonds (that conform to Climate Bond Initiative Standards) goes towards financing buildings, as compared to other countries in the region.

(Source: Climate Bond Initiative)

Laurent Margoloff of ING Bank N.V. in Singapore a observes a trend for increasing investments in energy and resources efficient and more largely green buildings in the region.

There is increasing focus towards green buildings as construction and operations of buildings accounted for 36% of global final energy use and nearly 40% of global energy-related carbon dioxide emissions in 2017. Through construction and retrofitting of green buildings, cities will be able to reduce energy and resource consumption, allowing them to achieve sustainability targets. This can in turn facilitate a greener and more liveable environment.

From the perspective of the private sector, there are also cost savings for adopting green buildings. Singapore’s City Square Mall, a 9-storey commercial building, has eco-friendly restrooms are equipped with “very good” to “excellent” fittings under PUB’s Water Efficiency Labelling Scheme. Motion sensors are also installed in their basement car park to control the lighting level. The adoption of green features in City Square Mall has resulted in an expected annual energy savings of S$2 million

![[Image] City Square Mall,](/-/media/InfraAsia/Insights/Green-Finance-in-Emerging-Asia/City-Square-Mall--image.ashx)

City Square Mall, which is the first retail mall in Singapore that received the BCA Green Mark Pearl Award, benefited from substantial cost savings from incorporating multiple green features.

(Source: City Developments Limited)

The ability of green buildings to potentially translate into higher asset value also increases appeal for green buildings. Based on a study on LEED certified buildings, green buildings can increase in asset value by 7% over time as compared to an identical non-certified office asset. Moreover, the returns of investments from green buildings in Asia are paid back relatively quick in less than seven years.

Considering the humid weather in majority of countries in emerging Asia throughout the year, green building regulations would have to take such climatic conditions into account to ensure buildings will not compromise on the living and working environment for its occupants. Singapore’s BCA Green Mark Scheme, introduced in 2005, is tailored to tropical and sub-tropical climates, thus enabling it to be a more suitable standard for green buildings in emerging Asia. This is reflected by the reach of the scheme, with close to 300 Green Mark projects in 80 cities overseas. The standards have gained popularity even beyond Singapore, with building owners from Malaysia, Indonesia, Thailand, Vietnam, the Philippines, China, India and the Middle East applying for Green Mark certification.

Challenge: International and Regional Standards of “Green”

Even though countries in emerging Asia are embracing green infrastructure, a challenge faced for green finance to flow more is the lack of a common green taxonomy. This has led to reservations on the lack of transparency and clear framework to measure how funds are used and if its usage is indeed “green”. This has propelled various green standards and principles to emerge to provide guidance for lenders and borrowers.

The International Capital Market Association’s Green Bond Principle (GBP) was established to promote transparency and disclosure of the quantitative determination of green bonds. The GBP has a robust framework that is based around four core components, namely the use of proceeds, process for project evaluation and selection, management of proceeds and reporting. The APLMA Green Loan Principle (GLP) further builds on to the GBP to facilitate consistency in the green loan market. The GLP was developed to provide a consistent methodology for use throughout the green loan market, which comprised of recommended guidelines on what is categorised as “green” in the green loan market.

In the ASEAN region, the ASEAN Green Bond Standards (AGBS) has catalysed the green bond issuance and provided guidance for ASEAN issuers in 2018. One key differentiating point of AGBS from other green standards is the development of a green asset class in line with the importance of green finance in supporting sustainable growth in ASEAN, targeted to meet ASEAN’s infrastructure needs.

Tan Chee Wee from DBS Bank explained that these principles broadly mention eligible green project categories in energy efficiency, renewable energy, pollution prevention and control, climate change adaptation, etc. They, however, do not provide a technically robust classification on what constitutes “green” and detailed definitions are still left to the issuer to determine.

Aligned with best global practices, corporate issuers are encouraged to engage second party providers and third party assurers, such as Sustainalytics (Sustainalytics is a leading independent global provider of ESG and corporate governance research and ratings to investors) and some of the Big 4 accounting firms, have established services to provide their framework and assessments on various green bonds and loans. For instance, Sustainalytics can provide a second party opinion to confirm that an issuer’s Green Bond Framework is aligned to the Green Bond Principles and to offer insight on market best practices and investor expectations. 89% of global green bonds issued in 2018 received external reviews, which includes second party opinions and green bond rating. This allows them to instil confidence and reassure investors that green bond proceeds are going to be allocated appropriately, thus raising the adoption of projects in emerging Asia through green financing.

Sustainalytics was engaged as the second party provider for the S$100m green bond issued by City Developments Limited (CDL), which includes funding for retrofitting and upgrading projects for Republic Plaza in Singapore. After undertaking the retrofit projects for Republic Plaza from 2010 to 2015, an estimated of 2,939 tonnes of carbon dioxide was reduced annually.

The Republic Plaza Green Bond issued in April 2017 – the first green bond issued by a Singapore company

(Source: City Development Limited)

Opportunities in Emerging Asia

Green bonds and loans have the ability to connect green-conscious investors and financiers to green assets, creating an opportunity and need for projects in emerging Asia.

Laurent Margoloff from ING Bank N.V. sees the potential for green and sustainable infrastructure in major ASEAN economies, including Indonesia, Malaysia, Philippines and Thailand.

Jakarta has committed to reduce its emissions by 30% from 2005 levels and to source 30% of its energy from renewable sources by 2030. An IFC report has identified close to USD30bn investment opportunity for the capital city, particularly in green buildings, electric vehicles, and renewable energy.

Thailand is another market that there are opportunities. After establishing its first green building in 2007, growing awareness of the significance and benefits of green buildings has led to the rapid increase in green buildings in Thailand. In 2018, ADB and B. Grimm Power issued Thailand’s first green bonds of $152 million. This issuance is an important development as it displays international best practice for green bonds and propels the country further into the green bond market in the region. More recently, BTS Group issued a Climate Bond Initiative certified Green Bond for the expansion of the monorail network in Bangkok in 2019, in which the second party opinion was provided by Sustainalytics.

In the Philippines, the topic of green finance is gaining traction, though the country is still in its infancy stage in terms of the volume of green bond issuances.

Nicholas Gandolfo from Sustainalytics shared that there is significant potential for the green and sustainable finance market in the Philippines to grow (as well as other parts of ASEAN), based on various transactions that they have been discussing with banks and firms.

Stella Saris from Australia and New Zealand Banking Group (ANZ) has also been observing a strong interest from the regulators, bank association and stock exchange on increasing sustainability reporting in the Philippines. With the build-out of infrastructure in the Philippines, including airports, green loans could be a financing solution for the country. Such financial instrument is possible as observed in the A$1.4 billion Sydney Airport sustainability-linked loan that ANZ arranged earlier this year.

Conclusion: Runways for Green Finance in Emerging Asia

Even though green financing is starting to be prevalent, many enterprises in the ecosystem still lack the awareness and knowledge of how green finance and green projects can benefit them. Thus, it is important for key “green” players in the public and private sectors to raise awareness on this topic by engaging the region in capacity building. Consistent efforts must be made to educate various stakeholders to understand and be involved in the green finance market.

Esther An from City Developments Limited highlighted that green financing has grown significantly over the past few years, which offers an alternative financing stream and plays a pivotal role in channeling capital to build greener and more climate-friendly infrastructure. Given Singapore’s relatively early adoption within the region, it is in a good position to share the relevant knowledge and ideas with other potential corporate green bond issuers or loan borrowers in emerging Asia.

With a robust ecosystem and Singapore-based players consisting of consultants, architects, developers, third-party certification firms etc., Singapore can share how the total package can come together to enable more green finance.

This article was collated by Seth Tan and Koh Sze Yen, and benefitted from the sharing of the following contributors:

- Esther An, Chief Sustainability Officer, City Developments Limited

- Laurent Margoloff, Director, Wholesale Banking – Utilities, Power & Renewables Asia-Pacific, ING Bank N.V.

- Nicholas Gandolfo, Associate Director, Sustainable Finance Solutions – APAC, Sustainalytics

- Stella Saris, Director, Energy & Infrastructure, Loans & Specialised Finance, ANZ

- Tan Chee Wee, Head of Sustainability Reporting, DBS Bank

References

- Asia Pacific Loan Market Authority & Loan Market Association, Green Loans Principle

- Asian Capital Markets Forum, ASEAN Green Bond Standards

- Asian Development Bank, 2015, Asia's Booming Cities Most at Risk from Climate Change

- Building and Construction Authority, 2008, Business Case for Green Buildings in Singapore

- Building and Construction Authority Singapore, 2017, Singapore firms expand overseas and strong building demand

- CDL Sustainability, April 2019, CDL Final Bond Allocation Report

- Climate Bonds Initiative, 2018, ASEAN Green Finance State of the Market 2018

- Climate Bonds Initiative, 2019, BTS Group Holdings - Climate Bonds Initiative

- Eco-Business, 2015, Singapore’s new Green Mark scheme a ‘game-changer’

- IFC, 2018, IFC Report Identifies More Than $29 Trillion in Climate Investment Opportunities in Cities by 2030

- International Capital Market Association, Green Bonds Principle

- International Energy Agency and the United Nations Environment Programme, 2018, 2018 Global Status Report: towards a zero-emission, efficient and resilient buildings and construction sector

- Olam International Limited, 2018,Olam International secures Asia’s first sustainability-linked club loan facility of US$500.0 million

- Royal Thai Embassy, Washington D.C., 2018, ADB and B.Grimm issue Thailand’s first green bonds

- Solidiance, 2013, Thailand's Green Building Goals: Aspirations VS Realities

- Sunseap, 2019, Sunseap seals first green loan for rooftop solar projects in ASEAN with ING

- The Business Times, 2019, Singapore looking to grow its sustainable finance sector: Heng

- United Nations Environment Programme and DBS, 2017, Green Finance Opportunities in ASEAN.